CFOs Guide to Business Valuation

A PwC report found that 70% of mergers and acquisitions fail due to misvaluations or misalignment between buyer and seller objectives. This emphasizes the need for CFOs to conduct a thorough business valuation.

When Is a Valuation Needed?

CFOs are often called upon to assess a company’s value in situations such as:

- Fundraising

- Share option schemes

- Acquisitions

- Taxation

- Shareholder exits

Valuation Challenges

Each business has unique factors—market sector, customer base, culture, and more—that make a one-size-fits-all approach impossible.

Strategic Valuation in Transactions

During fundraising or M&A, each party uses valuation methods that align with their goals, such as revenue growth, market share expansion, or acquiring technology. An accurate valuation is key to navigating these complex transactions successfully.

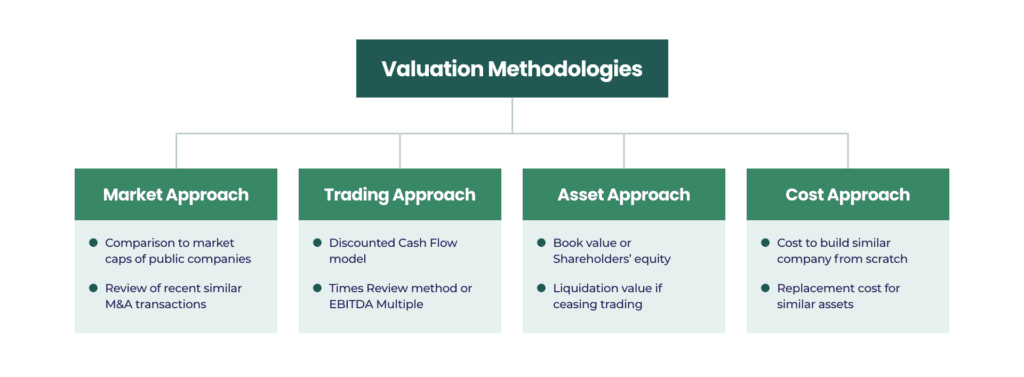

There are a variety of valuation methodologies that companies can use to determine the value of a business. These fit into the following categories:

The Importance of Multiple Valuation Methods

No single valuation methodology is perfect. Each has its strengths and weaknesses. By using multiple methods, CFOs can create a range of estimates that offer a reasonable indication of a company’s value. This range, combined with other factors like the importance of the deal to each party, helps in negotiating a final value that is acceptable to everyone involved.

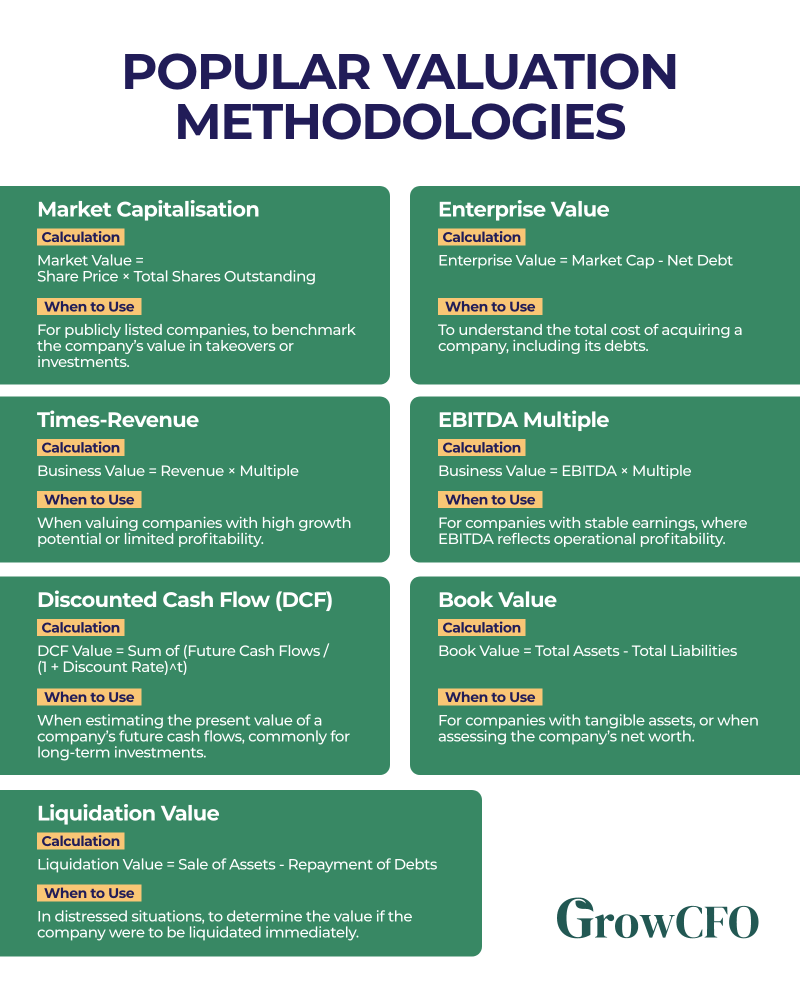

Popular Valuation Methodologies

Here are some commonly used methods for determining a business’s value:

- Market Capitalisation: The stock market value of a listed company, providing a benchmark for assessing the value of a potential takeover.

- Enterprise Value: The market cap minus net debt, indicating the cost to buy and fund a company.

- Times-Revenue: A method where the company’s revenue is multiplied by a set multiple to determine value.

- EBITDA Multiple: This method multiplies the company’s EBITDA by a chosen multiple.

- Discounted Cash Flow (DCF): A method that estimates the value based on projected future cash inflows, adjusted for inflation.

- Book Value: The value of shareholders’ equity, calculated by subtracting total liabilities from total assets.

- Liquidation Value: The amount of cash received by selling assets and repaying debts if the company were liquidated today.

By considering multiple valuation methods, CFOs can navigate the complexities of business valuation with greater confidence. However, it’s crucial to remember that shareholder transactions are not just about numbers—they’re also negotiations between buyers and sellers. While valuation calculations are key, factors such as the buyer’s motivation and the seller’s willingness to sell also play a significant role in the final outcome.

Ready to take your finance expertise to the next level and drive transformative change? Join us at the Future CFO Program Preview Event to unlock the strategies, tools, and insights that will shape you into a visionary leader. Don’t miss the opportunity to advance your career and achieve long-term success.